Introduction

Economics is a social science that aims to understand and describe how wealth is produced, distributed, and consumed. Thus, economic issues are a focus of the discipline. It aims to provide systematic answers to a wide range of issues involving the economic behavior of people, society, and the economy.

Definition

Numerous adjustments have been made to the definition of economics over time. Numerous economists have contributed to the subject’s increasing depth of meaning. Starting with Adam Smith, who is regarded as the founding father of economics. According to him, “Economics is the science of wealth” His theory emphasised materialism and had a narrow view of wealth.

Then came Alfred Marshall, according to him “Economics is the study of mankind in the ordinary business of life”. with his conception of welfare. His definition featured key points such as:

- Study of mankind.

- Study of the ordinary business of life.

- Study of material welfare.

- Emphasis on requisites of well-being.

- Exclusion of Non-economic activities.

However, despite all the improvements made to his idea, it was still criticized. This was due to the materialistic and unrealistic categorization of activities.

After Marshall, Lionel Robbins proposed his definition- “The science which studies human behavior as a relationship between ends and scarce means which have alternative uses”

For his definition, Robbins got both praise and criticism. His work was praised for providing a reasoned justification for economic issues. He even said it had a universal nature. He said that it was a human and positive science. The term gave a broader perspective on economics.

Finally, Paul. A. Samuelson’s definition is the one that many economists still accept today. The Growth-Oriented Definition was his idea. Economic issues were emphasized in the definition. It had a long-term outlook and a flexible strategy. His theory addressed a wide range of issues. It covered all bases and took a wider angle.

Thus, even as a topic, economics has had a hard road to building its foundation.

Real-world examples of economics

To better understand economics, some broad or real-world examples can be used.

Example 1 – Opportunity Costs

Opportunity costs are the advantages that a person or corporation forfeits by selecting a different course of action. Typically, not all possibilities are taken into account while choosing, which results in a number of opportunity costs being missed or overlooked.

Consider a company which had extra capital that they could either invest in the stock market to earn an annual return of 15% or update its equipment to earn an annual return of 12%. If the company chooses to upgrade its equipment to make higher-quality items instead of investing in stock it will forgo a return of 3% (15%-12%). The opportunity cost to the company is this 3%.

Example 2 – Sunk Costs

A sunk cost is a cost that the company has already invested and cannot recover. It is a prior expense incurred by the company that is not taken into consideration while making future business choices. When making decisions for the future of a business, sunk costs remain constant.

Imagine you go for a movie, and it turns out to be terrible but since you have already paid for the ticket, you tend to sit and watch the whole thing. Through this, you don’t realize that watching the movie is not going to get your money back. However, we end up wasting our time.

Example 3 – The Trade War

Every country makes an effort to safeguard its own economy, companies, and industries. They would protect the interests of the businesses in the country as local industry generates jobs. As a result, when commodities/goods are imported from other countries, they impose greater tariffs and taxes. In response, the other nations impose even greater duties. This creates a conflict known as Trade wars.

The best example of this is the ongoing trade conflict between the United States and China, in which the US imposed higher taxes on commodities/goods imported from China and China responded by imposing comparable duties on US goods.

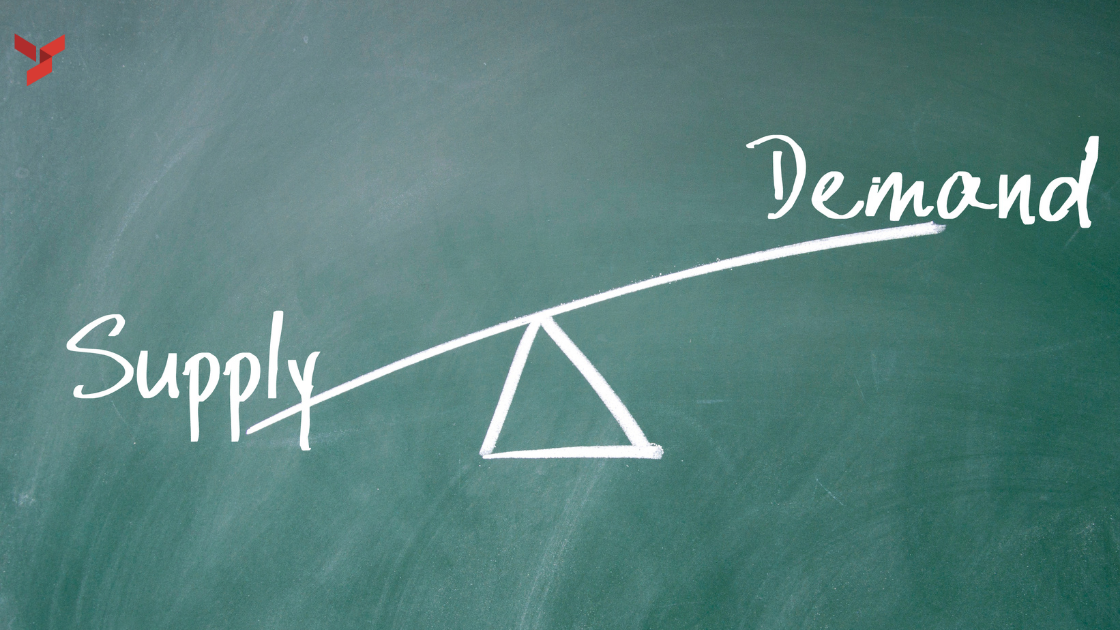

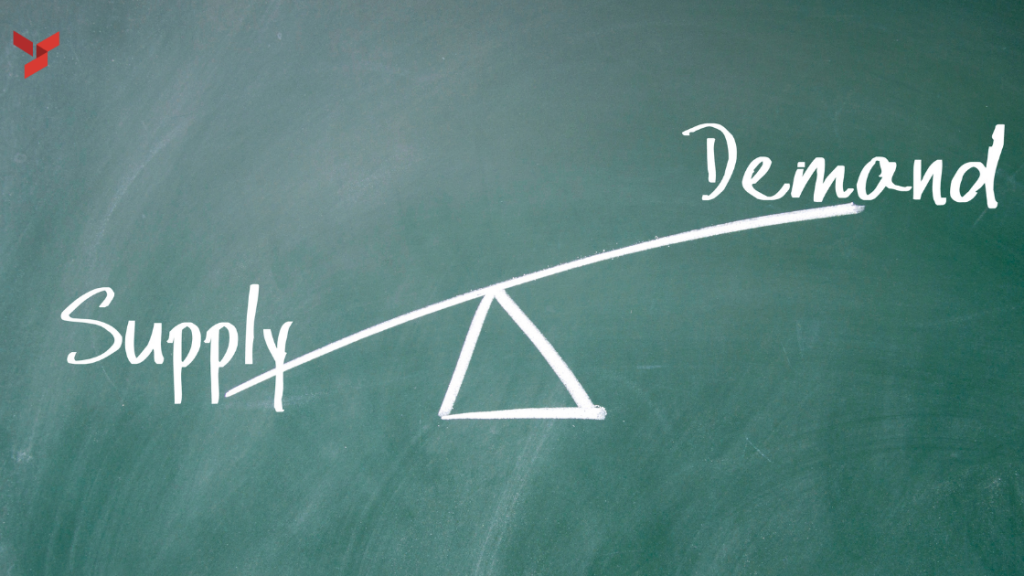

Example 4 – Supply and Demand

Economic theory is based on the rule of supply and demand. Demand is the quantity that market participants are willing to purchase, whereas Supply is the number of items that producers float on the market. The equilibrium point is the location where supply and demand are equal enough to satisfy one another, it is where the supply and demand curves meet in an efficient market.

For example, Farmers lower the price of the crop when corn production rises in order to sell more of their harvest. When there is an excess of supply compared to demand, the produce is wasted and the farmer is at the loss of their cost of production.

Conclusion

The above examples give an overview of a few of the concepts of economics, which include the law of supply and demand, opportunity costs, sunk, and trade wars. Though they do not cover all types of variants; it does give a fair understanding of real-world economics. For more understanding of Economics, register with us at Young Scholarz and book 1:1 sessions with our certified Economics tutors for IB and IGCSE.